It's a LST world we live in

Liquid Staking Tokens are the hottest topic of 2023.

Why is it? ETH being the second most capitalized crypto and the home of smart contracts means that almost everyone is affected, which makes the stakes very high and puts the ethics of Ethereum at the center of the debate.

Let’s dig in.

First things first, why stake ETH?

An absolute majority of crypto users hodl ETH. ETH now offers a yield through POS staking, something that was inaccessible without a dedicated and costly infrastructure under POW. But is it profitable for every type of users to stake ETH?

Not exactly, but we are getting there real quick. Gas fees paid when staking can eat up months of yield for small wallets (< $1000), so it didn't make much sense for them to stake until Layer 2s were functional.

Presently this problem is almost solved now because small wallets can buy ETH LSTs on rollups depending on liquidity with low gas fees and therefore make staking much more profitable.

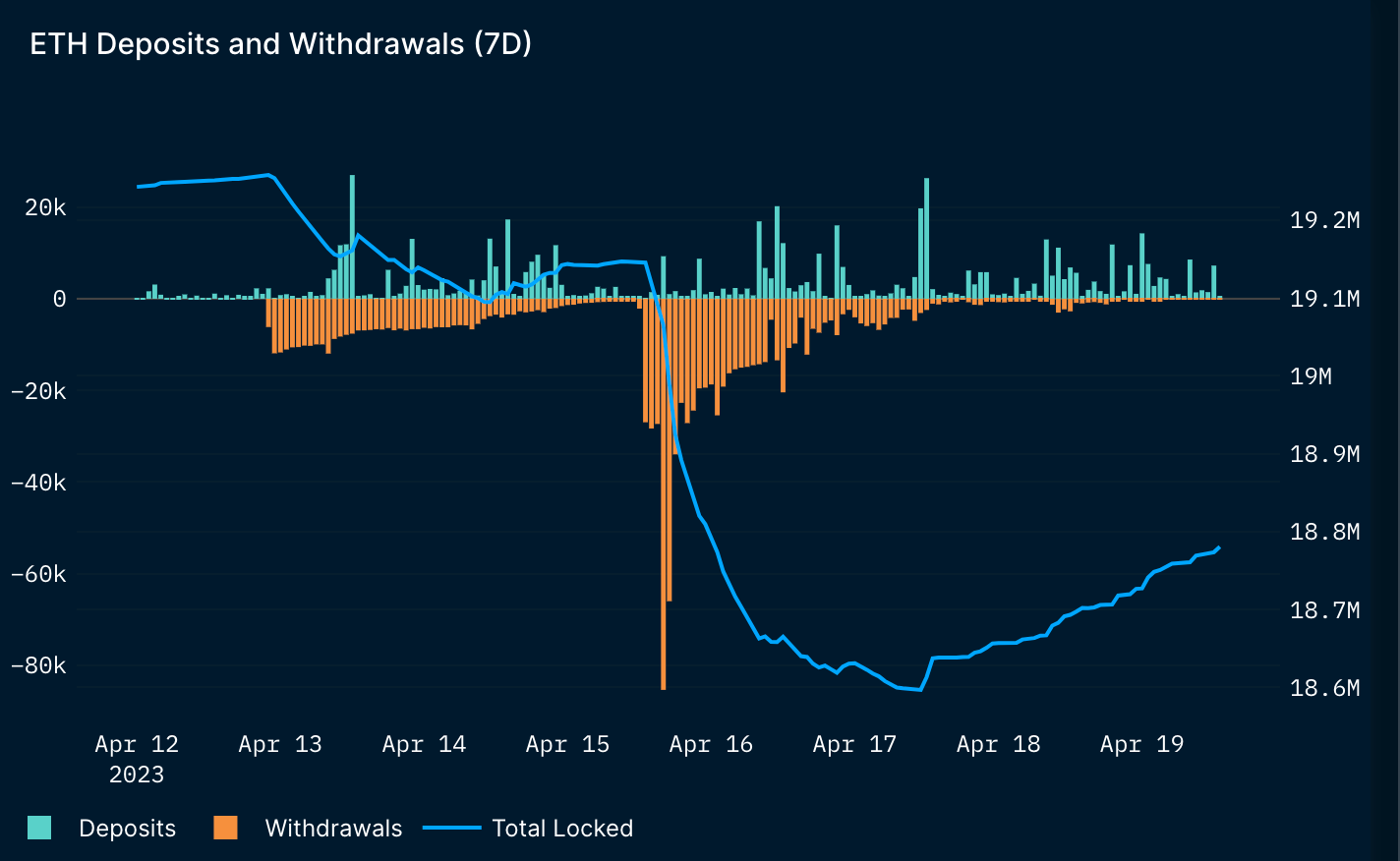

With Shapella implemented, you cannot be serious about hodling naked ETH.

I'm not the only one thinking this, the trend of ETH net inflow is now up after the logical wave of withdrawals. This trend has everything it takes to stay up only.

Bridges was the essential infrastructural piece to allow some activity in the upside down. LST are the essential piece to bring ETH staking for everyone.

So lots of LST have swarmed on Ethereum since 2020. Of course the main ones are no longer a mystery to you, I’m talking about stETH by Lido, rETH by Rocketpool, sfrxETH by Frax for the decentralized options and cbETH by Coinbase for the CEX one.

Here is the top 10 by TVL thanks to Defillama :

So the obvious question is what is the best staking option?

There is no clear cut answer to this. I tweeted last time that LSTs targeted different ETH holders profiles and that was a good thing.

I think we can separate ETH holders in 3 main categories :

the ones who want to run nodes in a permissionless way to be involved in the security, execution and decentralization on the Ethereum network

those who simply want to generate a competitive yield on ETH in a decentralized fashion

people who are only seeking the highest yield on ETH in DeFi

First category

Potential new nodes operators will likely choose to run validators directly without third-party involved. With the required technical knowledge, it’s the most profitable option and one that is most in line with the ethos of Ethereum.

But what if the staker that want to run a validator only have 25 ETH and not 32?

Currently there is only one protocol that solves this problem. It’s Rocketpool.

On Rocketpool, you can create validators with only 16 ETH. The protocol loans the others 16 ETH to a node, then the 32 ETH validator is created.

Where these 16 ETH came from? Users looking to stake ETH without running validators can deposit ETH in a pool and earn yield from the Beacon chain minus a commission, their ETH is then used to fund the validators’ creation. Under Rocketpool’s architecture, a validator is called a minipool.

The node operator will pay half of the yield earned to the protocol while taking a commission of 15%. The node operator gains the capacity to run a validator and earns 16% - 42% more than a solo staker. It’s a fantastic win-win for everyone.

This model has been proven PMF as Rocketpool amassed almost $1 billy in ETH distributed among 2311 node operators at the time of writing.

But it’s now even better with the very recent Atlas upgrade. This introduces minipools LEB8’s which means that if you can assume configuration, maintenance and high performance of your node, you can run validators by providing only 8 ETH (+ some RPL). I encourage you to read the details on the Atlas Upgrade after you finish reading this, it’s interesting.

So current node operators can run two times more validators if there is enough ETH available in the deposit pool and the entry cost to run a node has been divided by 60%. Massive.

How Rocketpool make it permissionless?

There is no job interview to run a node and you don’t need anyone’s permission unlike Lido. It only requires the infrastructure and a high level of performance to not get slashed. Post Atlas, transitioning from a solo validator to a Rocketpool node operator can be frictionless by simply setting your withdrawal address. There is no need to exit the validator during the process. 85 179 validators (14.8%) have not yet set up their 0x01 withdrawal address, it would be nice to see how many switch directly to Rocketpool.

To protect the protocol and ensure node operators act of goodwill when starting a minipool, Rocketpool requires that a minimum of 10% of loaned ETH be provided in RPL as insurance. So it’s an additional cost of 1.6 ETH in RPL for the start of 16 ETH minipools and 2.4 ETH (30%!) for 8 ETH minipools.

If the nodes performs badly, the RPL stake will be slashed. To compensate this additional investment, they earn ≈ 8% APY on RPL thanks to the token inflation (5% annual). So the price of RPL is a function of staked ETH growth on Rocketpool therefore RLP has a “floor” and utility. Interesting.

Others protocols don’t compete in this area as they don’t offer this type of deal to potential node operators for now.

Rocketpool takes the win in this category. On to the next one.

Second category

Now the spotlight is on those who want to stake and earn a competitive return on ETH in a decentralized way.

I can see 3 main factors in play : the yield of the LST, its decentralization and its liquidity. I’ll focus on the yield later as it’s the main aspect of the 3rd category.

Decentralization

Rocketpool is ahead of the others with its 2311 nodes as Lido has only 29 node operators, the Frax team runs all the validators for the moment. Coinbase stated that they have diversified trusted node operators similar to Lido but I can’t find data on this.

I note that Lido has more unique stakers (194k) than Rocketpool (11k), Coinbase (17k) and Frax (2.2k) combined. I don’t think it really matters if the same few nodes run the majority (all?) of the validators as launching new validators increase the randomness of block proposals but doesn’t make the protocol more censorship resistant.

Frax and Lido need to do better on that aspect. Lido seems on the right path as a pilot integration of Distributed Validator Technology is currently running on Goerli testnet. The idea of DVT is to bring validators together into independent committees that propose and attest blocks together, greatly reducing the risk of an individual validator underperforming or misbehaving. Thus, authorized and unauthorized node operators can do their jobs together.

Frax is also working on its own DVT model but we don't know much yet. SfrxETH growing rapidly, the process must not take too long to get started as this would create too much friction in ETH migration once permissionless node operators are accepted.

Liquidity

Lido’s stETH is out of this world due to its first mover advantage and the Lindy effect. You can swap 100’s of millions of stETH through liquidity pools on different decentralized exchanges. At time of writing, the stETH/ETH Curve pool has $1.63b in liquidity which allows only a 0.42% price impact on a 50 000 stETH > ETH swap. Impressive.

RETH has about $188m of liquidity mainly through Balancer ($89m on mainnet), Uniswap and Curve spread over different networks.

FrxETH has 171m$ across various DEXes with $156m in the frxETH/ETH Curve pool.

CBETH has $65m overall with $48m on Balancer.

Shapella upgrade makes liquidity less important as you will be able to unstake directly on the protocols. But unstake can lead to delays if your size is size (welcome to the withdrawal queue) which can be inconvenient depending on the need of the user.

Regarding deposits, stETH doesn’t have a minting limit unless you deposit 150k ETH a day à la Justin Sun. FrxETH doesn’t have a limit either. The Rocketpool deposit pool has a fixed limit of 5k ETH, once reached, ETH must be loaned to the nodes so that minipools can be created to empty the pool and authorize new rETH mints.

So deep and balanced liquidity pools are still needed and Lido is unbeatable on this ground for now.

Currently frxETH is very competitive on the LST yield but not on the decentralization aspect, rETH struggles to keep up in the yield’s competition due to its hefty 15% commission taken on the yield and paid to node operators.

As a result, Lido offers the best combo between decentralization, liquidity and yield for people who want to stake without running validators.

Third category

That of ETH holders who only seek the highest ETH yield in DeFi.

It’s a frxETH world we live in.

SfrxETH brings the highest yield thanks to the smart dual token model concocted by Frax. It need to be seen if the yield can keep up with the supply’s growth as the CVX voting power of Frax is insane but not infinite, especially now that frxETH is looking to replace WETH to become the currency of DeFi. This involves a classic Frax program, namely matching emissions of pools paired with frxETH in proportion to the TVL they bring to frxETH.

However I’m not too worried about that as sfrxETH should be pushed as the main product of Frax, potentially to the detriment of the stablecoin someway. I think this is the right way to go as sfrxETH shows the path to decentralization for FRAX, added to the fact that regulatory uncertainty is putting pressure on FRAX's growth.

The main competitors don’t have enough voting/bribe power to offer a yield higher than their respective staking return as providing roughly the same yield to LPs is already costly for non-rebasing LSTs. Moreover the rapid growth of LSTs dilute the non-staking yield.

My guess is that the gap in yield between providing liquidity to LST pools and the staking APY will widen as the need for protocols to incentivize liquidity to maintain LSTs’ peg has shrunk with Shapella. Arbitragoors can do their job frictionlessly now.

Let's see if an increasing adoption of LSTs and therefore more volume generated can sustain the yield of the liquidity pools. FrxETH & sfrxETH can do well in that context if LST volumes don’t grow much because the dual model forces Frax to incentivize the frxETH/ETH Curve pool a lot.

Layer 2s

Smaller wallets will use rollups to buy LSTs with low transaction fees so they don't lose half of the yield just by getting in and out.

Rollups liquidity :

- stETH : $21.5m on Arbitrum & $15.9m on Optimism.

- rETH : $63m on Optimism, $888k on Arbitrum.

- frxETH : $5.33m on Optimism, 0 on Arbitrum.

- cbETH : 0

Overall liquidity is quite low except for rETH. This makes sense because liquidity must already be incentivized on Mainnet at high cost, so sizeable transactions should take place there. Liquidity is still sufficient to allow retail to buy their favorite LST with low slippage.

Non-rebasing LSTs can bring IL to their pools, but this is more than offset by trading fees if you do the math. Maybe it's a bias still present in LPs’ minds that slows them down.

I expect more liquidity coming on layer 2s because a large part of the DeFi’s activity must migrate there in order to make DeFi more accessible, more capital efficient and innovative.

Making staked ETH the standard ETH on rollups should be a collective goal.

Composability

Stakers who are looking for the highest yield are not hampered by leveraging the yield, at contrary. So they need a liquid lending market for the LST they choose.

Based on Defillama data, rETH, sfrxETH/frxETH and cbETH don’t even have one lending market on Optimism or Arbitrum while available liquidity for wstETH is relatively low.

Leverage can reshuffle the cards for the highest yielding LST award, so it might seem odd that few options are available.

Of course, liquidity plays a role but there is another determining factor, the Chainlink price feeds. We observe that frxETH & sfrxETH don’t even have a chainlink price feed, the rETH price feed is not verified yet, while it’s all good for wstETH and cbETH. This is a problem because having the price feeds of these LSTs will considerably secure the use of these assets, which will facilitate the arrival of fresh capital and new lending markets.

The native Arbitrum and Optimism bridges support wstETH, rETH, frxETH and cbETH, so there is no issue on this side.

Protocols like Concentrator on Ethereum offer auto-compounding and the possibility to choose the blue chip token in which the yield will be paid. But for these options to be worthwhile, they need more LSTs pools’ incentives to compound.

The rollup market is up for grabs for LST protocols. With the war being less intense here and everything relatively new, the opportunities to gain significant market share are real. rETH also seems to believe so with high liquidity already available on Optimism.

FrxETH is the winner in the 3rd category, no one can really compete on the pure yield aspect and the numbers show it. SfrxETH pays 5.05% APY while second-best stETH only offers 4.3%, a spread of almost 15%.

So Rocketpool for the ETH holders who want to run nodes in a permissionless way.

Lido’s stETH for those who want to generate yield on ETH in a decentralized fashion.

Frax’s sfrxETH for the people only seeking the highest yield on ETH in DeFi.

Choose your fighter.

Which category has the most ETH to allocate post Shapella?

Logically the first mentioned, that of holders who want to run nodes. They know they can safely withdraw now, and especially they are the first concerned by the migration of CEX stakers. Users of other categories didn't really receive an influx of fresh ETH as withdrawals were available to them via LSTs liquidity on DEXes.

I think CEX staking is in trouble except for Coinbase as cbETH will be the entry point to ETH staking for Americans (and even that, with the SEC you never really know). Kraken’s ETH staking lost some user confidence, Binance always gives the impression of having a sword of damocles hanging over its head. The others will never be considered as viable long term options. The probability of having a problem with a CEX is higher than that of a smart contract’s critical bug or a hack on one of the main LST protocols.

A slow but certain migration should therefore begin from CEX to LSTs. For instance, this is already happening on Kraken as all ETH staked by Americans must be withdrawn (551 000 ETH) thanks to the SEC.

ETH whales on centralized exchanges will enter unchartered seas and go decentralized. Logically the majority should chose Rocketpool to easily create validators and gain more yield than elsewhere thanks to the 8 ETH minipools model. Whales should not have issue with infra cost as the extra yield earned on their size offset it.

LSTs’ aggregators/index need also to be followed closely as some users may simply not want to choose between the LSTs. If an “index token” offer a higher and better risk-adjusted yield than other staking options on a high time frame, these would become very relevant.

I’m thinking about yETH here, the unborn baby of Yearn Finance. The model consists of a basket of LSTs which have fixed allocations determined through vote by the st-yETH holders. These holders will bootstrap yETH by depositing ETH in the yETH vault and lock it for 16 weeks. Once the selection and allocation of LSTs have been defined by the genesis votes, the ETH in the yETH vault will be used to buy the LSTs. The model looks promising and Yearn Finance has massive veCRV voting power to offer decent yield to the yETH/ETH pool. The potential is obviously there.

UnshETH ($33m TVL) is an index of LSTs with target allocations determined by a decentralization ratio set by their community to fight against a monopoly of an LST.

Agility ($366m) is trying a different model with a liquidity distributed platform that acts as a composable vault to bootstrap liquidity for new LSTs. There is a stablecoin to borrow against LST liquidity. The rationale is that the combination of token incentives by the LST and Agility should give more visibility and value to a new LST.

For the time being, these new models are attractive mainly because of their high token emissions, bringing the yield of LSTs to around 15-20%. We'll see if they really are PMF once emissions decrease and get less valuable.

You know I'm a Conic fan, so of course an ETH Omnipool with only LST pools inside would make a lot of sense. This can offer exposure to the trading fees of the LST Curve pools which are a proxy of their adoption. This is an exchange of a portion of the exposure to the yield from the beacon chain for that to the yield from trading fees and incentives. Firstly, the main LST pools must meet the Omnipools’ requirements in terms of oracle (the chainlink price feed again) and liquidity. I'm sure this will be implemented in the not so distant future.

The liquid staking token that becomes the leader in 2 of our main 3 categories is likely to take it all. It will be fun to monitor because at first glance the current leaders of each category have a lead that seems unrecoverable.

Anyway, all this war serves only one goal..

I try to write shorter papers but as you can see I failed kek.

Thanks for your time, I hope you enjoyed.

Daesu