Secure the yield

Part one.

In today's high rate environment, securing the yield is a mantra. The Fed's interest rate is 5.5%. The fed pays 5.5% per year for you to lend them money. If your annual returns are below this crucial level, you're better off not investing at all and just parking your money at the Fed. Before you only had to outperform inflation, now you have to outperform inflation and the Fed interest rate.

This profit threshold has contaminated crypto. As we are in a pre bull market, sustainable and predictable profit opportunities are rare. So rare that we decided to fulfill the RWA narrative and import treasuries yield on-chain as a cheat code.

Where does the yield come from?

The primary source of yield in crypto is the ETH staking yield which is highly correlated with Ethereum usage. It's not predictable, but it has a floor that is around an average gas price of 7 gwei over a year (assuming fixed skated eth supply and price). If activity is even lower than that for such a long period, we will have to question many things.

Then you have borrowers and traders who are the only users paying fees 24/7 to protocols (and to Ethereum). When it’s getting hot, they don’t hesitate to pay more to trade or borrow, always looking for the best returns available. When it's cold, they fight for relatively high, sustainable and predictable yields. These behaviors define the economic models of the crypto ecosystem. They generate yield for lenders and liquidity providers. Very functional but not very predictable.

Yet these primary sources of yield are the closest forms of sustainable yield in crypto.

So we use them. These are our weapons to outperform the Fed.

Demand is quickly absorbed in crypto, even more so in a bear market because opportunities are rarer and demand is lower. If there is unusual borrowing or trading activity that generates a high yield opportunity somewhere, people will quickly deposit liquidity to take advantage of the situation and fill the gap created. This happens faster in bear markets because liquidity is concentrated in a few safe places, unlike in a bull market where no one really cares if they miss out on another 10%, meaning liquidity is spread everywhere.

For the connoisseurs, if the crypto market was a tournament, it would be a Grand Slam during a bull market and a Master 1000 during a bear. The difference is that the level of the playing field is more concentrated and so higher with fewer matches, points and money to be won but enough to make it very attractive for the top tennis players.

Market participants must therefore sharpen their weapons to be competitive.

"Leverage has entered the chat".

Outperforming the Fed requires leveraging yields until our majors decide to lead us towards utopia. Leverage is inevitable, that’s our DNA. We did it, we do it and we will do it. Whether it's good or bad doesn't really matter. If the source of the yield is pure, you just have to act as a responsible ape and not get liquidated.

I won't talk about our ultimate leverage weapon, crvUSD, because in its current configuration it only allows us to take advantage of the volatility of the underlying asset and not its yield (you cannot borrow the same type of assets). Its time will come.

Two newcomers caught my eye to help us accomplish our mission. Pendle and Lybra. Each with their own character trait, each allowing them to secure and leverage the yield of deFi, and not that of treasuries.

This article will be separated into two parts. As people are more familiar with Pendle, let’s start with Lybra.

Lybra

My focus is on the v2 as it’s the current deployed version. The v2 underwent 3 audits (Code4rena, Consensys and Halborn).

Lybra is a stablecoin issuer. The stablecoins issued are called eUSD and peUSD and are pegged to the US dollar. The price is hardcoded to $1 in the protocol.

To mint them, you need to open a loan in a permissionless way collateralized by an ETH liquid staking token. Max LTV is 66% right now or a collateral ratio of 150%. Minting eUSD seems free at first glance. I’ll come back to this later.

1 eUSD or 1 peUSD is redeemable against 1$ worth of ETH LST (liquidity depends on the rebase yield accumulated and the redemption providers).

But nothing new innit?

There is a twist. In this model, you are highly incentivized to mint eUSD and not peUSD. Minting eUSD is only available with stETH, a rebase LST. Because the borrowers sacrifice their staking yield, Lybra can redistribute this yield to the eUSD holders.

EUSD being a rebase stablecoin, the method used to distribute the rebases is a little complex. The rebases aren’t printed they are bought. Generally, this happens once a day few hours after the stETH rebase but someone needs to trigger the rebase. In fact anyone can buy the excess generated stETH tokens of the vault with eUSD, the shares of the profit are then burnt in favor of every eUSD holder, which increases their balances due to the token’s rebase nature.

Previously this was done by the team and the ETH/USD price is retrieved with an internal oracle. Of course, this wasn’t very decentralized nor trustless. But it wasn’t really their fault as the incentives to do that were inexistent for users. Ameliorations regarding this process were expected for v2. The team executed and now there is a fresh incentive to trigger the rebase, a dutch auction of the excess stETH in the vault offering a 1% discount every 30 minutes. It is accessible through UI. MEV bots are likely in charge of the rebase redemption since v2.

The game theory assumes that minters don’t like liquidation risks therefore they will likely mint at a CR around 200% and maintain it. If it’s the case, and it is, the stETH yield generated by the collateral will only feed half of the value is supposed to if held in a wallet. So at 200% total collateral ratio, you earn 2x the stETH yield just by holding eUSD. The higher the TCR, the higher the eUSD yield. The floor of this yield is the minimum TCR, ie 150% or 1.5x the staked ETH yield. Currently the TCR is around 180%.

Of course, earning that much “guaranteed” yield has a cost for the eUSD holder which comes in the form of a 1.5% tax on all eUSD in circulation. I was intrigued to know how much stETH was still used as collateral in defi to measure the boundaries of this market for eUSD.

There is $1.05b worth of stETH used as collateral on Aave v2, elsewhere wstETH dominates without sharing. It’s still a lot of stETH that can earn a higher premia on Lybra.

As this model has scaling limits due to the rebase LSTs, peUSD was introduced to allow minting with non-rebase LSTs. Less game theory this time, borrowers keep their staked ETH yield because it is only realizable at exit under this form (wstETH, rETH, wbETH). As eUSD, peUSD is an ERC20 but doesn’t earn any yield.

peUSD was thought of as the composable version of eUSD, the one that can be cross-chain and employed in deFi (liquidity pools, collateral). So to compensate the loss of the stETH rebase yield for Lybra, peUSD minters must pay 1.5% in interest when they close their loan.

Was it necessary to create two stablecoins just to do that?

Yes I think so. Remember that one of the main benefits of Lybra is getting a rebase yield on a stablecoin that is higher than the yield of the staked ETH. If you kill eUSD exclusive minting through rebase ETH LST, you kill a main value proposition. Also the rebase design makes it a pain in the ass to integrate eUSD deeply in deFi.

So to add the peUSD composability to eUSD, a simple trick has been done. When you convert eUSD to peUSD through the protocol, your eUSD stack acts like a vault where peUSD is the receipt token of it. This way you can earn the eUSD yield while using peUSD in DeFi. The eUSD rewards are still accumulated daily but will be inaccessible until you cash out your yield gains when you close your “vault.” (burn peUSD to get back eUSD+accumulated yield).

Logically, it’s impossible to convert peUSD to eUSD through Lybra if you haven’t firstly take the path from eUSD to peUSD. Because you chose to keep your staked ETH yield, you can’t have that of others.

So peUSD minters could be in front of a gigantic yield opportunity: combine peUSD’s yield in deFi to the safer and more sustainable eUSD yield.

These days, holding eUSD yields around 5.5% without doing anything else. There are also liquidity pools on Curve as eUSD/3CRV which contains $15m and yields 8.5%.

The highest yield opportunity for peUSD resides in the peUSD/USDC Curve pool (on Arbitrum) which yields 9.4% apy on Lybra. This is a cool use case of the OFT component of peUSD. The collateral stays on Ethereum, the eUSD rebase yield is earned on Ethereum while also providing liquidity for peUSD to earn yield on Arbitrum.

13.4 millions of dollars sit in the pool on Arbitrum, ie. 56% of the 19.3m peUSD in circulation (the pool is imbalanced).

PEUSD needs more pools to expand its supply, I think about pools paired with LSTs to improve the slippage on a potential leverage, or to pair peUSD with sDAI or sFRAX to offer high and diversified yields opportunities. There is also a lack of auto-compounding solutions for peUSD. Regarding the collateral use case, it could take time as peUSD need to establish a proper oracle, sufficiently deep liquidity and some time.

LBR

Lybra designed its governance token LBR as the way to get 100% of the protocol’s revenues but also a boosted yield on your mint value.

To earn the protocol revenue, simply stake LBR to esLBR.

But actually, how does the protocol make money?

Do you remember the 1.5% tax on all the eUSD circulating supply? All of it is distributed to esLBR holders in eUSD or USDC.

Do you remember the 1.5% interest rate paid by peUSD minters? All of it is distributed to esLBR holders in eUSD or USDC.

eUSD or USDC because it depends on the eUSD price. If it trades above $1.0005, the fees earned would be sold for USDC and distributed as it to suppress the premium.

All of this put together push revenues to $1.66m annualized based on current data.

This carries the esLBR APY to over 20%. The figure is impressive given that the yield is organic, paid in stablecoins and already 33% of the circulating supply is staked.

To earn the incentives of the mint pool whose value is represented by all minted eUSD, you need to secure at least 2.5% of your loan value in dynamic liquidity provisioning (gm radiant), ie. in LBR/ETH uni v2 LP tokens.

LBR/ETH liquidity, now at $7.6m, has been boosted to the point where a sale of $10,000 in LBR for ETH only generates a price impact of 0.56 %. Impressive.

The yield is high

But there is more. If you lock your esLBR from 1 month to 1 year, you can earn a multiplier on the mint pool’s yield that goes from 1.05x to 1.5x. To get an idea of the max boost requirements, assuming the current total loan value of $121m, a loan of 100,000 eUSD and 7.8m esLBR, 6459 esLBR need to be locked for one year ($5555 at $0.86 per LBR). This is 5.5% of the mint value.

Now it’s getting crazy. The mint pool yields almost 17% without boost. So with the 1.5x max boost, it’s possible to earn 25% apy (paid in esLBR) on your eUSD and peUSD minted.

So by minting eUSD you can literally secure the yield by earning:

5.5% apy paid in eUSD by holding eUSD

+

9% apy paid in esLBR by converting eUSD to peUSD and LPing it on the Curve pool

+

25% apy on your eUSD paid in esLBR

+

1.1% apy paid in eUSD, peUSD or USDC coming from esLBR locked to max boost

cumulative apy earned : 40.6%

costs:

1.5% of your loan value for protocol fee

2.5% of your loan value for dLP (in LBR/ETH LP)

5.5% of your loan value for the max boost (in esLBR)

cumulative costs : 9.5%

The premia is currently around 31% on eUSD ie. 15.5% on the staked ETH deposited at a reasonable LTV (50%). Without any leverage.

Assuming LBR loses 50% of its value, you would still earn a premia of 10.6% on eUSD.

This is clearly one of the most interesting yield opportunities on the market.

Advanced vesting

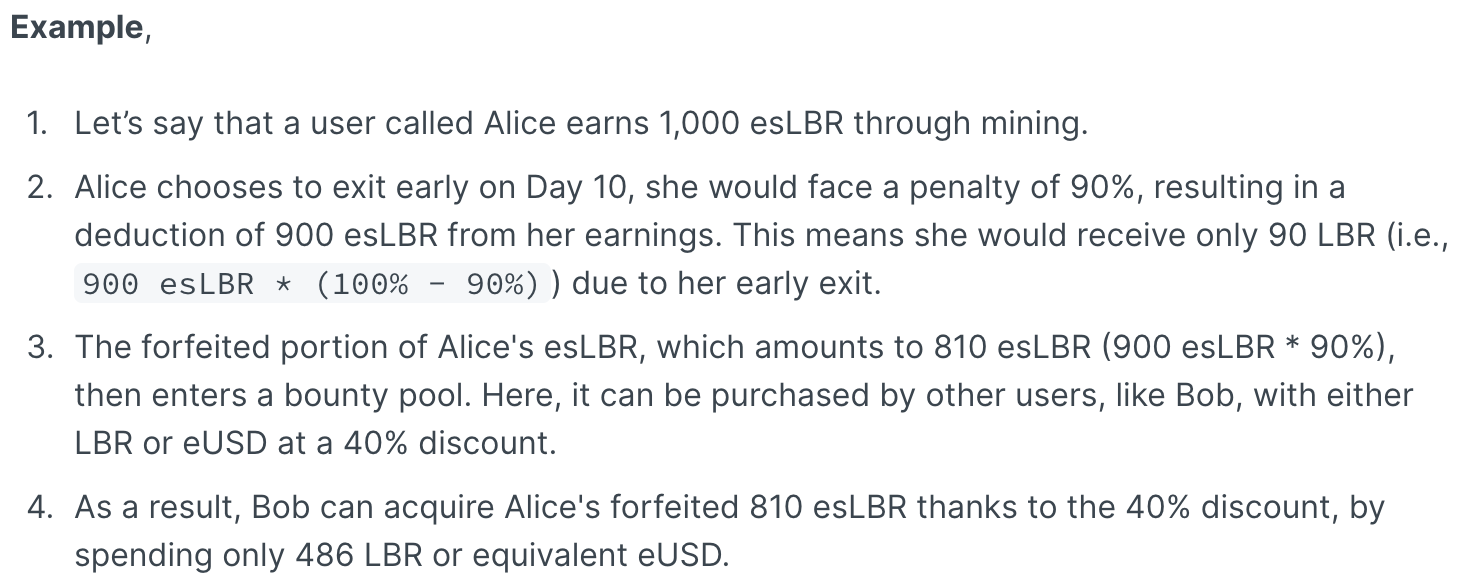

What is even more interesting is that you can buy esLBR at 40% discount.

How? Once earned, esLBR has a 90 days vesting period. If you can’t wait, you can exit early and get your LBR back for a 25-95% penalty based on the vesting time remaining. Buyers can buy the esLBR that you sacrifice at 40% discount with eUSD and LBR.

The LBR acquired by the protocol through these buys is 100% burned while the eUSD is kept in reserves to serve as a stability mechanism. So far 109k LBR have been burned.

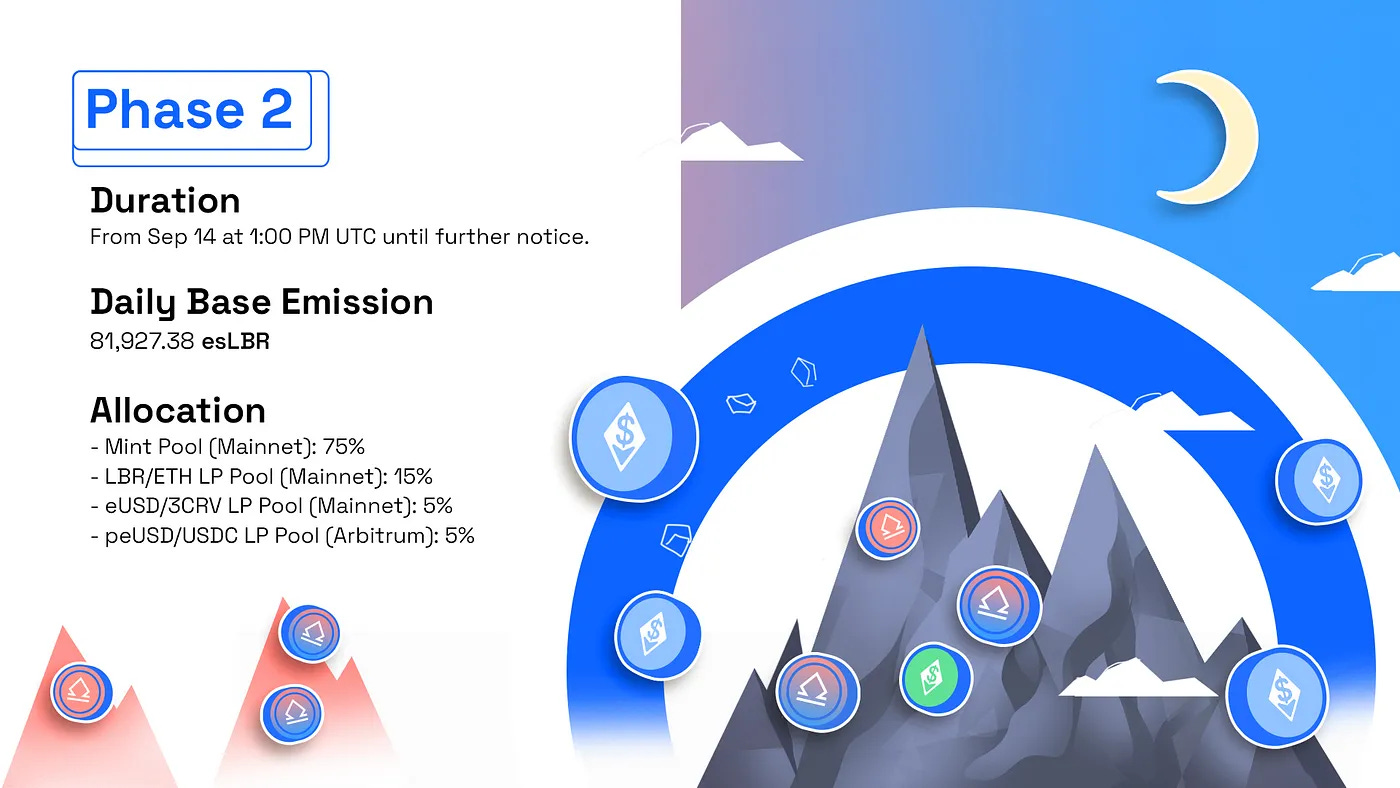

LBR design is smart and seems to work fine despite the delirious amount of 81 927.38 esLBR distributed daily (29.9m annualized or 2x the circulating supply). 60m LBR or 60% of the total supply will be distributed through liquidity mining during the next two years. Emissions’ value is critical as they represent 80% of the maximum achievable yield for eUSD (without costs). I don’t see this figure decreases anytime soon.

According to this dune dashboard, LBR market cap is around $12m, there are 14.4m LBR in circulation which 7.8m are staked as esLBR (33.69%).

This chart proves that there is organic demand for LBR. Whether it’s for a dLP or to enjoy the protocol revenue. Additionally, esLBR's 90-day vesting period alleviates potential selling pressure that can arise from the high emissions.

Note that advisors already unlock 375k LBR per month and the team will unlock 354k LBR per month from the end of this month. The team may need to reassure the community about what will be done with these tokens.

Especially since partly founded questions have arisen concerning a flow of LBR dumped on exchanges for a assumed total of $2.5m during the summer. The team justified this under operational expenses and preventing front running. I consider this story to be bullish long term because the quantity announced was size so they won’t do it again before a long time. More important, the price is still holding up well.

My perspective on this project would not be the same if the price action was different, but I can feel something special here, of course this could end very well or very badly if the price ends up breaking under the weight of its emissions.

I almost forgot to talk about how eUSD try to maintain its peg to the dollar.

Over-collateralization - current TCR is 186% ($207m deposited and $111m borrowed) - minimum TCR is 150%

Arbitrage opportunities when eUSD <$1 or >$1 - redemption against 1$ worth of LST

The availability depends on the accumulated LST yield (primary liquidity source for redemptions) and redemption providers - RP earn an extra 10% yield in the mint pool by making their collateral available to be sold for eUSD.9% liquidation fee + liquidations through flash loans - the eUSD locked when eUSD is converted to peUSD is available to be used to facilitate the liquidations.

Stability fund – using eUSD acquired through protocol fees and advanced vesting to primarily sell eUSD when it is above its peg in order to remove the premium.

eUSD is trading at a premium right now, which isn’t surprising and similar to the behavior of LUSD in the early days. It’s the issue when your stablecoin is well designed and possesses enshrined utility. People mint a lot of it but don't sell enough, which creates a premium.

Let's see if over time the mechanisms to bring eUSD back to the peg work well enough (this requires a sale of 5.6m eUSD). In my opinion, this arbitrage stays because someone who just want to close it need to pay 1.5% as a fee to Lybra, hurting a vast majority of his potential profit at the current price of $1.02. The constructive approach would be to offer higher yield to the liquidity pools to generate more selling pressure and more eUSD minting, which would also increase protocol fees and protocol’s firepower to sell eUSD above 1$.

peUSD is trading at a discount, which is also not surprising. This is likely because there is not enough LST liquidity to redeem enough peUSD to re-establish the peg. And peUSD minters aren't paid to hold peUSD so they'll likely sell at least 3/4 of it to provide liquidity and earn yield.

The yields are high but somehow sustainable as shown by the cute uptrend and the quantity of eUSD in circulation which tickles $100m.

Governance

The Lybra DAO launched recently and the first proposals are discussed. Obviously it’s a good thing to accentuate decentralization. Discussions to add new collateral are underway (swETH, ETHx, far from done).

The first snapshot proposal closes today. It concerns the destiny of 2m LBR that didn’t migrate yet to the v2. The popular option gives 3 months to v1 LBR holders to migrate to esLBR v2 against a 3% migration fee distributed entirely to the v2 esLBR holders.

The impact will depends on how many v1 tokens migrate to the v2. But it could dilute the esLBR staking yield (by a max. 25%) and increase the required esLBR amount to get the max boost.

I need to say that there are also some serious issues to fix, as having a chainlink oracle for LBR/ETH (it’s coming) to calculate more precisely the dLP value, and to retrieve LST prices through chainlink data price feeds or more robust oracles. Currently the team utilizes a built-in price feed for LBR/ETH and updates it manually. They can do much better. So there is a lot of potential but also certain aspects which raise questions. There is more good than bad here in my opinion.

Regardless, this model is interesting because it takes advantage of the lack of capital efficiency in the case of over-collateralized loans. The yield is redistributed differently, improving the attractiveness and capital efficiency of a stablecoin at the same time. This way, the yield you earn is correlated to your risk curve.

For more details and infos on Lybra, don’t hesitate to DYOR (docs, audits, discord).

I still have a question for you.

What if you liked what you read but you think the staked ETH yield will decrease further or the TCR will reduce, leading to a reduction in the eUSD yield?

It seems the only solution is to pray or not ape and potentially miss out on a crazy return. In an ideal world, the idea would be to find a way to secure the current yield because you find it overvalued over a horizon of 6 months to 1 year.

“Pendle has entered the chat”.

Thanks for your time. This is not a financial advice. See you for part 2.