Secure the yield

part. 2 - Pendle has entered the chat.

What if you liked what you read but you think the staked ETH yield will decrease further or the TCR will reduce, leading to a reduction in the eUSD yield?

It seems the only solution is to pray or not ape and potentially miss out on a crazy return. In an ideal world, the idea would be to find a way to secure the current yield because you find it overvalued over a horizon of 6 months to 1 year.

“Pendle has entered the chat”.

This was my conclusion of the part one.

High yields are for many one of the fundamental values of crypto. But with every yield comes its share of questions. “Where the yield comes from?” and '“am I the yield?” are the main fears of deFi users. I provided some possible answers to these questions in the first part.

So, how to secure this sweet yield as long as it lasts? Imagine being able to earn the hundreds of percent of yields that were available during the bull run even on valuable assets. A lot of people would have love to secure that type of yield for at least a year.

During the bear, most of the yields opportunities have been destroyed due to their unsustainability (eg UST). Often these overvalued yields did not come from real activity and fees generated by real users, but from inflated and useless shitcoins rewards. One bear market later, the industry was forced to become more mature.

Now there are more sustainable yields available but harder to scale because they are more real. Opportunities are therefore quickly seized, mechanically reducing yields. So users need a way to secure it. Few models emerged to solve this issue, Pendle is simply the best in my opinion.

Pendle allows you to trade yield. Buy low and sell high is a mantra in crypto. Buying the yield low and selling it high could easily be a new one. But yields have been up and down for few cycles. So why is now the time?

This is a clear sign of the maturity of DeFi. No one would have built a protocol like Pendle if there were not enough sustainable returns that could be traded. Today it makes a lot of sense. The main reason is the Merge which brought us the most sustainable yield ever from ETH staking.

The explosion of the fed interest rate helped a lot too, accelerating the arrival of RWA and the 5% IORB rate on-chain. These two yield sources have one thing in common, public opinion thinks that they will eventually decline. Is it due to unsustainability or overvaluation? More the latter. No one wants to keep something overvalued unless it is not expected to be repriced at its fair value. Are the IORB rate and the ETH staking yield overvalued?

That's another debate, let's assume that we find them a little too high and therefore want to secure them before it’s too late.

I'm not going to dissect Pendle from top to bottom, I'll focus on the aspects that intrigued me the most. This is the AMM to trade yield, the Standardized Yield which offers the ability to separate a token from its yield and Pendle’s expansion limits.

Pendle’s SY

Trading the yield is great, but how Pendle allows you to trade yields that are generated differently by each protocol? It required a standard. Pendle built it.

GYGP

A Generic Yield Generating Pool is a pool on Pendle that contains all the assets deposited.

But these deposits aren’t under their original form in the pool, they are under the form of shares. The input tokens are converted into assets, eg depositing ETH into the Pendle’s stETH pool. These assets are converted to the underlying asset of the pool, stETH in our example. These stETH tokens will then be deposited into the GYGP pool to mint new shares. The exchange rate is obtained by dividing the total value of assets in the pool (total value of stETH deposits) by the total amount of shares. So deposits increase the exchange rate and withdraws decrease it. The depositor receives its share or SY stETH LP tokens. Basically, this is the receipt of its deposit into the pool.

In this way, the deposit can be converted from a set of input tokens to a single SY standard, the role of which is to ensure that a deposit which increases the total value of the assets results in a creation of shares of equivalent value at a given exchange rate. Now that this problem is resolved, we needed to find a way to distribute the rewards in the form of SY tokens equitably among the shareholders.

A subset of the GYGP was born, the Simple GYGP. The idea behind is that each time rewards are distributed to the pool, they are distributed equally among each shareholder based on their number of shares.

This allows the creation of a rewards token index that represents a state of the distribution of the pool’s rewards at a time t. By subtracting each rewards token index in the formula to determine the rewards received at time t by a user, Pendle will not distribute new rewards based on a user’s shares of the pools that is no longer current.

So if everyone use the SY standard, composability could increase a lot and the majority of the complexity of managing various yield-bearing assets could be eliminated. This allows for better accounting and easier integrations for money markets, vaults and aggregators.

SYS

Standardized yield stripping is the process of splitting a yield bearing assets into its principal and its yield. This mechanism works only on SY tokens and requires an expiry to mint PT and YT.

YT represents the right to claim the real-time yields until the expiry, and PT represents the right to redeem the principal after the expiry.

So, the yield stripping pool is introduced to complement the GYGP. The SY tokens acquired by depositing assets in the SYGP are then deposited in the YSP to mint PT and YT.

Mint and redeem PT and YT

When a YT token is minted by an user, a PT token is also minted at the same time. You can’t mint PT without minting YT and vice versa. So the value of the PT supply is always equal to the YT supply. In the pool, the SY tokens deposited earn the yield generated by the assets of the GYGP. This yield is then allocated equally to the YT holders until expiry. But it’s not distributed directly as it needs to be claimed.

Holding YT tokens will make you earn the same yield than holding the same value of SY tokens. Only the cost differs.

PT holders don’t receive rewards but still earn yield through another form. 1 PT token is only redeemable after the expiry for 1 SY token of the yield stripping pool, and so 1 asset of the GYGP pool. If the pool’s asset generated 0 yield during the period, 1 PT token will worth 1 asset from start to expiry.

YT token is also redeemable but requires the corresponding amount of YT tokens. When an user mints a PT token, he gets get the corresponding YT token. So buying PT is necessary to redeem the underlying asset. Equal amount of PT and YT token will be burned for SY tokens, then the SY tokens will be redeemed for the same amount of base assets in the GYGP. These assets finally arrived in the user’s wallet.

Pricing and correlation between YT and PT

Regarding the price of the PT tokens needed to buy, let say that 1 PT token is simply the receipt of one pool’s asset bought at discount, the discount value corresponding to the yield earned by one pool’s asset during the period. And so, the price of a YT token is just the representation of the yield earned by one unit of the base asset. That’s why PT and YT prices are correlated.

By simplifying as much as possible, we can say that if the yield of stETH increases by 10%, the price of the YT token will increase by 10%, decreasing the PT token’s price by 10%. I’ll try some scenarii that exclude fees and trading for simplicity.

Let’s assume that stETH yields consistently 10% apy and that the underlying rate equals the implied rate. A SY stETH pool is launched on Pendle on January 1st with an expiry set for December 31st (time t for one year = 1).

At origin, the price of 1 YT token is 0.10 stETH and the price of the PT token is 0.90 stETH. The price of the PT token is 0.90 stETH because the implied rate is 10%. This also means that 1 stETH SY = 10 YT stETH and 1 stETH SY = 1.11 PT stETH.

This is important because it’s how leveraging the yield works on Pendle. Buying 1 YT stETH at 0.1 stETH is buying the yield of 1 stETH. Thus, the lower the YT stETH price, the lower the cost of earning the yield of 1 stETH. In this case, the leverage is 10x.

To profit from buying and holding a YT token until expiry, the amount of rewards received should be higher than the amount spent in stETH to buy the YT token. For this condition to be met, the underlying rate must be higher than it was at the time of purchasing the YT token.

Logically, selling the YT token before expiry is profitable only if the yield earned during the hodling period added to the value of the PT token at the moment of selling is greater than the amount originally paid. So, buy low sell high.

Let’s go back to the example.

One hour later, the underlying rate (ETH staking yield) explodes to 20%. The YT token now worth 0.20 stETH and the PT token 0.80 stETH. Because YT market cap should always equal PT market cap, the price of the PT token adjusts to the increase in the underlying rate, even more when underlying rate = implied rate.

To identify the nuance, if the same yield variation occurred 6 months after the pool launch, the YT token price will increase from 0.05 stETH to 0.10 stETH, because just before the yield increase, holding YT token only yields 10% *0.5/1 until expiry. So, the PT token price will be 0.95 stETH before the increase and 0.90 stETH after.

If the underlying rate decreases from 10% to 5% one hour after the pool launch, the YT token price will reduce from 0.10 stETH to 0.05 stETH and the PT token will increase from 0.90 stETH to 0.95 stETH.

If the same thing happened six months later, the YT token will decreases from 0.05 stETH to 0.025 stETH and the PT will increases from 0.95 stETH to 0.975 stETH.

If the yield is flat over the year, the YT price will decrease slowly to 0 until the expiry. It is guaranteed that 1 PT token will worth 1 asset at maturity which implies that a YT token will be worth 0.

This mechanism slowly increases and decreases the price of each PT token to match the variation in YT market cap (in this specific environment). In the Standardized Yield Stripping mechanism, YT market cap + PT market cap = total value of SY tokens in the yield stripping pool.

Now I think we have a better view on the mechanisms of the PT and YT tokens and the impact of yield and expiry on them.

Now focus on trading the yield.

AMM

When you dig deeper into an AMM, the main thing you want to know is how the price moves when users buy or sell tokens, what model is used to define the slope of the curve, and what parameters govern it.

Who has the best model for trading yields?

Based on the whitepapers, a lot of work has been done to find the optimal model for the Pendle v2 AMM. The PT token AMM allows users to buy or sell principal tokens against the asset. The model chosen as baseline is the Notional AMM.

The formula used to price the asset in PT is very different from the geometric mean formula, property of Uniswap v2, and it’s more similar to the constant power sum formula from the YieldSpace model used by Yield Protocol. The main problem with the two models cited is that they aren’t customizable which means that every yield trading asset will have the same curve. Problematic when every yield is generated from a different source and so acts differently.

The main changes that makes the National AMM’s formula different are two parameters absent from others such as of the scalar root and rate anchor.

Scalar Root and Rate Anchor

To speak french, the rate anchor is similar to the underlying rate weighted by the time remaining until maturity. That’s how I understand it. Its goal is to maintain the flattest curve possible at the level where trading will be most capital efficient, ie. when the greatest proportion of PT tokens will have to be sold/bought to move the implied rate. It is notably thanks to this parameter that the price of a PT token will follow changes in the underlying rate. This is the level at which the implied rate should trade in normal conditions.

The scalar root is used to define the interest rate’s trading range of an asset. Its value is determined by some things that I can’t really understand but from my modest math level, I can say that the gap between the maximum rate that an asset is not supposed to exceed and the average expected rate plays a big role. This gap is negatively correlated to the value of scalar root. I will venture to say that it plays a role similar to that of the amplification coefficient of the famous Curve StableSwap model.

If the interest rate is expected to trade in a tighter range, a high scalar root value needs to be set up to maximize capital efficiency. The best example is the yield of stETH.

If the apy is expected to be volatile and so the gap between the max rate and the expected rate, the scalar root value will required to be set very low. The implied rate needs to react more quickly to the short term variations of the underlying rate, and this is realized by a higher price impact of the buys and sales of PT tokens. This means that the curve is sloppier than for less volatile interest rates. A good example would be an asset that offers 50-100% apy.

Implications

So, the Notional model with the right values of scalar root and anchor could work very well to price an implied interest rate against an asset and trade it through a pool.

Here are our curves in t = 0.5, ie. after a year of life for a pool containing cUSDC with a with a lifespan of two years. Max implied rate = 1.20 (20%) ; average expected rate = 1.09 (9%).

The range set up is from t =0.1 to t = 0.9. Close to the birth and the death of the pool, slippage is out of control. Y-axis represents the implied rate and the x-axis the time from origin until expiry (t = 1 being the origin). The curve represents the impact of the buys and sales to the implied rate.

The flattest curve from 0.1 to 0.9 wins, and it’s that of the notional model. Why?

The flatter the curve is over a longer period of time, the higher the proportion of the pool required to impact the implied rate price will be. This is essentially what you want for a trading pool of sustainable yield-bearing assets, that only significant inflows and outflows from the pool have a real impact on the implied rate.

If it wasn’t the case, the implied rate will be too volatile which creates barriers preventing us from having a good view of how the market actually prices the interest rate. Additionally, in yield trading, every percentage counts as profit margins are lower. Very low price impact is therefore necessary to maximize capital efficiency.

The graph speaks for itself and so do the test results.

Yes, you read correctly, 48-55 times more capital efficient than the closest competition.

After six months of trading, selling 11.6% of the pool or 116.48 PT stETH are necessary to dump the PT stETH price from 0.95 stETH to 0.94 stETH, which also means pumping the implied rate from 5% to 6%, ie. an increase of 1%. This one percentage is equivalent to a 1% price impact for the PT seller.

With other models, we navigate between 0.12% and 0.24% of the pool for the same yield variation. This is good. Crazy good. And you already understood how vital it is to offer the best trading experience to Pendle users.

It might be important to describe what happen under the hood when you buy a YT or a PT token as flash swaps are used. Remember, buying and selling PT and YT only impacts the implied rate.

When you buy YT stETH with stETH, the AMM takes your stETH, wraps it in SY stETH, “borrows” more SY stETH from the pool to match your quantity of YT tokens (your leverage). Then it mints PT and YT with all the SY, gives you the YT and sells the PT for SY stETH to "repay" the pool. The price impact is generated by the selling of PT tokens when the size is size.

When you buy 1 PT stETH with stETH, the AMM takes your stETH, wrap it to SY and sell 1 SY stETH for PT stETH at the exchange rate (1/implied rate - fees). Price impact could also be involved.

Selling YT involves the same process but in reverse (borrow PT from the pool to redeem SY, give its part to the seller and buy PT with a portion to repay the pool).

Same reverse process for selling PT.

If you don’t want to suffer price impact, you can always mint them both.

Liquidity providers

Regarding adding liquidity, it’s similar to a classic Uniswap v2 pool, you deposit SY stETH and PT stETH based on the current distribution of the pool and there you go. This way a liquidity provider to the SY stETH pool can earn the staking yield on part of its deposit and the implied staking yield on the other part. Added to this are trading fees and incentives allocated towards the pool. Sweet.

Note that the markets needs to be bootstrap at launch by locking forever a part of the initial deposit.

To avoid IL when withdrawing liquidity, LPs should wait until the PT stETH is at a lower price than when they acquired it, otherwise they’ll realize a (very) low IL by selling or redeeming the PT token for stETH before expiry. The price impact plays its part too.

Interesting studies carried out by Pendle prove that IL is greatly attenuated without PENDLE incentives and completely erased by including them. Of the pools analyzed, the IL was 0.85% in the worst case (without incentives).

Regarding risk profiles of the liquidity providers, I think they should be bullish on the ETH staking yield, because logically in a bear there’ll be more PT buys than sales and so the pool will quickly be unbalanced in favor of SY stETH. LP tokens will contain more SY stETH, making their yield more influenced by variations in the underlying rate.

Currently, there are 19% SY stETH and 81% PT stETH in the pool which expires on December 25, 2025. This pool yields 6.2% right now. Trading fees only represent 0.16% of the yield and PENDLE incentives weigh 42%. The liquidity position can received a 2.5x max boost if the necessary amount of vePENDLE is held. So even if a LP isn’t bullish on the yield, these incentives can compensate for his exposure to a possible reduction in the yield that he has already anticipated by depositing into the SY stETH pool.

I’m not sure how the pools’ liquidity can scale at big size as LPs must have a divisive opinion on the yield evolution over a long period.

One word on the zero price impact mode which is a good solution to onboard large LPs. When providing liquidity without this option, the YT stETH minted with part of the deposit are sold against PT stETH (price impact generated) in order to be deposited in the pool with the rest of the SY stETH. In zero price impact mode, the minted YT are not sold for PT but given to the depositor. Only the minted PT stETH and the rest of the SY stETH will be deposited into the pool.

So, part of the Pendle AMM magic resides in the Notional model’s parameters scalar root and rate anchor, and above all in the correct setting of their values.

Now that we see more clearly in all this, we know that trading almost all yield-bearing assets efficiently and securely (without price manipulation) is possible on Pendle, let’s focus on the limits of Pendle. This will allow me to also talk about some trading strategies on Pendle.

Pendle boundaries

Let me be clear, now that I deep dived on Pendle, I am very bullish on it for the present and the future. By the way, an underestimated criterion for knowing if a project is really good is the simplicity of its white paper when you really take the time to read it. Pendle's is very clear regarding the complexity of the concepts explained. I can say the same thing about the crvUSD whitepaper (the second version lmao).

Pendle the Fed of crypto

Back to Pendle limits and some crypto fiction, I think that Pendle could play a role similar to that of the Fed. I am crazy? Maybe, but when you can control the short end of the yield curve, you can have an impact similar to that of the Fed on the bond market.

The rates of the crypto bond market would be defined by the staking yield of ETH and the on-chain representations of the IORB rate, then the variation of these yields will impact the behavior of market participants and their perspective with regard to risk.

if a drop in the ETH staking yield is anticipated, the implied rate of the stETH on Pendle should decreases first. If the Pendle market is sufficiently liquid to be efficient. And it will soon be the case if things continue like this.

Some market participants will anticipate the yield decrease and try to benefit from it. Previously there was no way to do that in size in a trustless way. Now with Pendle, you can simply buy PT stETH. Secure the yield.

A high profit opportunity attracts size and so the price of PT stETH will go up, decreasing the implied rate ie. the exchange rate of 1 stETH against 1 PT stETH (excluding fees). But you already know this if you were focused.

How do we move from that to the Fed-like role?

The great self-fulfilling prophecy of the markets. If Pendle's staked ETH market is worth billions of dollars and demonstrates its desire to price the implied interest lower by an aggressive purchase of PT tokens, it may be right. This could impact the behavior of ETH stakers because this new information may encourage them to unstake to chase higher yields before the crowd.

You know how mass effects work, and the traditional bond market often gives us nice examples. So where is hiding this higher yield? Logically in the on-chain Treasury yield.

Treasury yield should be very high when the ETH staking yield is way lower than its average because the treasury yield is somehow correlated to the activity on Ethereum, and so to the staking yield. If everybody is in T-bills, who’s using Ethereum?

This is the current status quo and at the speed at which treasury yield is being incorporated on-chain, it's likely only a matter of time before the relation increases further.

But for now it’s only relation between these rates, not a direct negative correlation yet. The assumption is that a high treasury yield discourages investments in risky assets, meaning people do not seek outsized returns by trading altcoins. You all know that Uniswap takes first place among energy guzzlers. So this reduces the activity and ETH staking yield at the same time.

Crypto fiction

Now’s the time for crypto fiction. Let’s assume that staking adoption increases, LST and lido market share also. Now the SY stETH pool has $3B worth of stETH in it. When the market anticipates a decline in the staking yield, at least $1B worth of ETH is leaving DeFi to be put into Pendle to buy PT tokens. Out of DeFi means out of Uniswap, Curve liquidity pools, Aave or Maker, disrupting trading conditions and therefore Ethereum activity. Now the correlation is direct. To mitigate this and keep that billion in fee-generating ETH, PT stETH could be used as collateral.

There is a world where the next evolution of staking ETH via an LST is to stake it via its SY pool, with the ultimate collateral being SY LST LP tokens or even crazier, something like a stETH omnipool including a mix of SY LST LP tokens with different maturities.

What if ETH holders can't part with their staked ETH yield or are bearish on t-bills? They’ll secure the yield. As they aren’t bearish on the staking yield, they could just stay in staked ETH but they know that nothing can be done against the mass in fine, and they’ll just see their yield melt away. So even if they aren’t bearish on the yield, they aren’t bullish on it, so the ideal place for them is somewhere on Pendle. The race to buy PT tokens, oops I mean bonds, to suck up the yield and crash the implied rate even more.

All this movements will impact to a lesser extent the long end of the yield curve. It will depends on the market conviction that the staking yield will stay lower longer. Doesn't that remind you of anything? Same old shit, just a different asset class.

So Pendle allows to recreate the yield curve on-chain and Pendle users can take control of the short end of the yield curve.

I would have liked to develop more this Fed analogy, on the tokenomics, the short term catalysts and obstacles, the incentives, how to make Pendle more permissionless, but you have already read around 4700 words. Maybe in a third part, who knows?

I can’t leave without giving you the three best yields opportunities on Pendle.

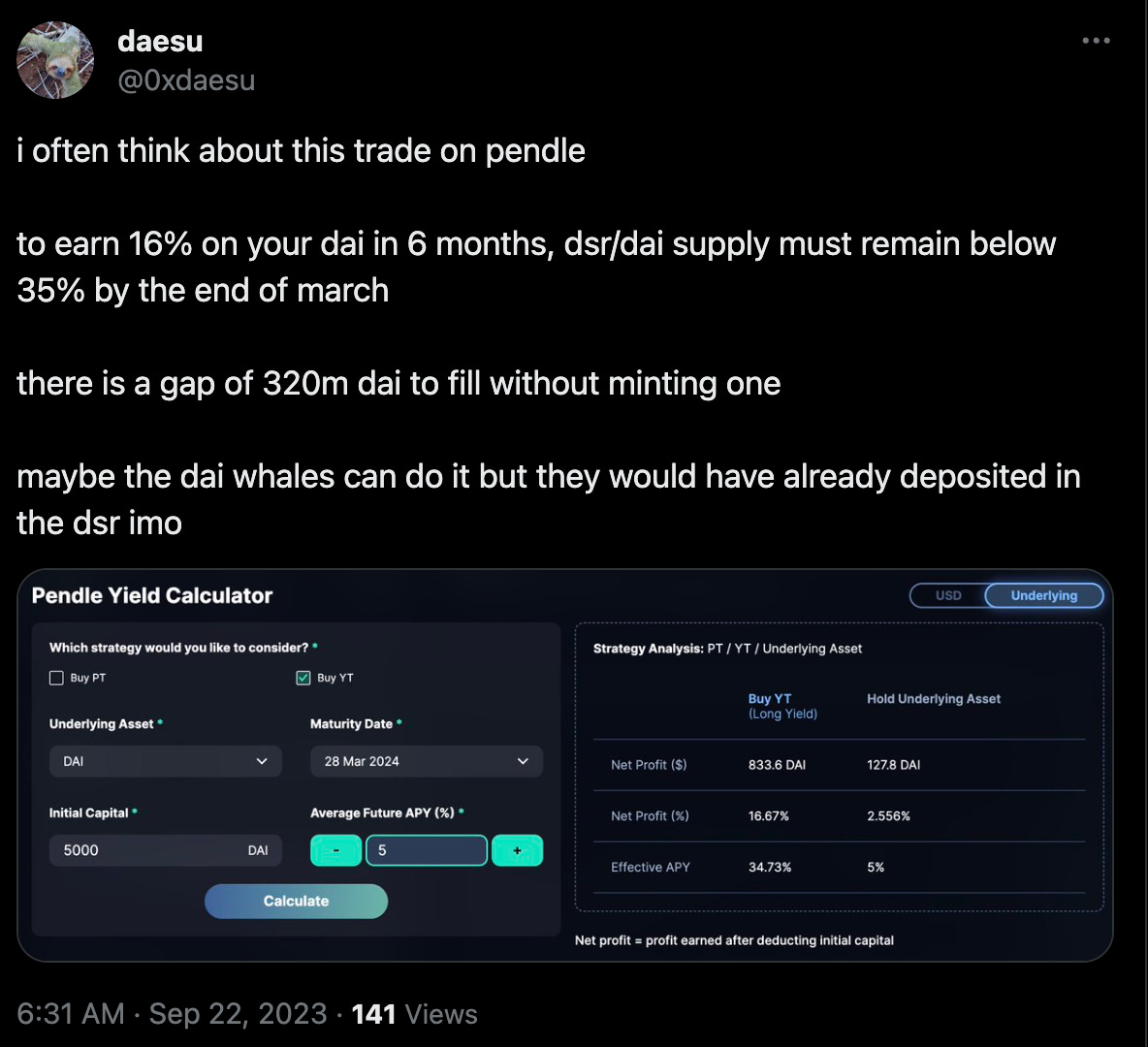

1- the best trade was to buy YT sDAI (expiry 03/28/2023) one month ago but the net profit has been divided by 4. The risk reward is no longer worth it. For the same trade at September 2024 expiration, I believe the DSR will have decreased in the meantime due to the 35% ratio being exceeded.

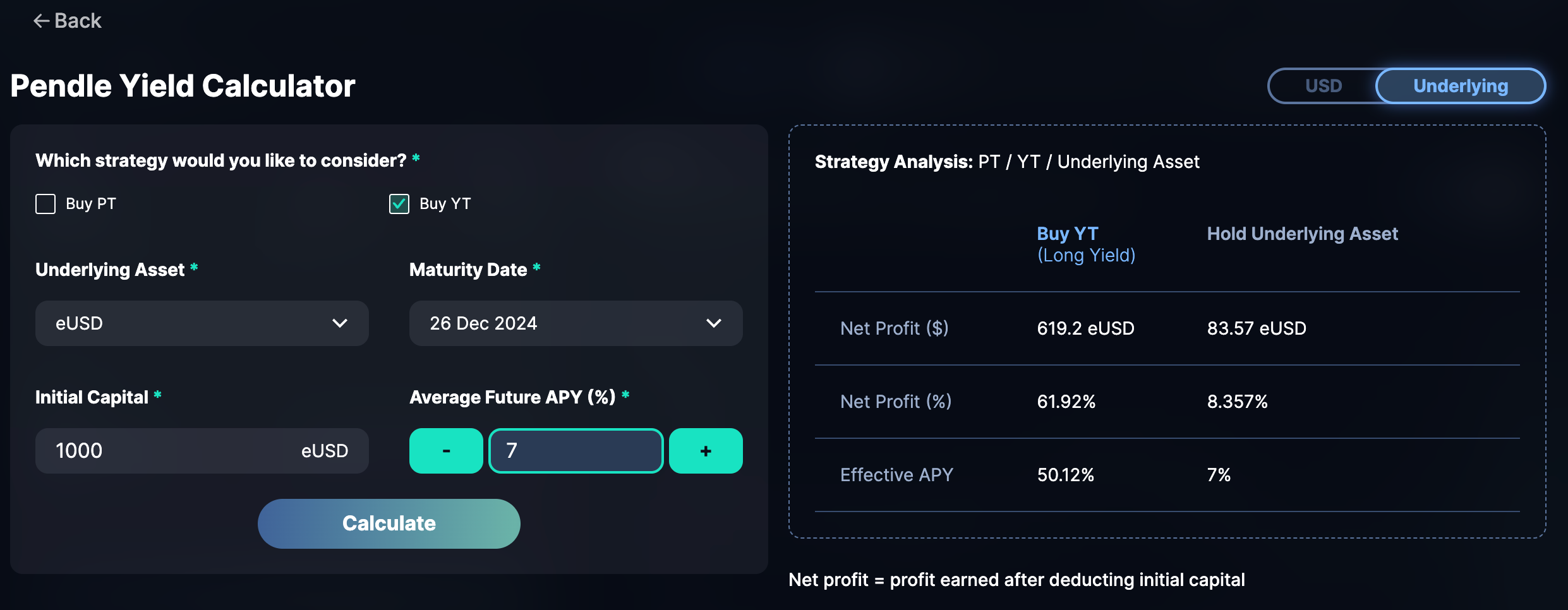

2- Buy YT PT eUSD (expiry 12/26/2024) and sell when the implied rate is repriced higher than 7% - if there is indeed a bull market in 2024, the ETH staking yield should take off, and the eUSD yield is a beta of that yield, as the eUSD supply earns approximately 2x the yield of stETH (part one if you don’t understand)

3- buy YT fUSDC (expiry 12/26/2024) and hodl until maturity. Ondo is doing a great job and OUSG gets traction. The only way to borrow is to finance through Flux Finance with fUSDC at 92% LTV. There is $170m TVL of OUSG and only $34m deposited on Flux. Almost all the USDC is borrowed (90% utilisation rate) and supplying USDC yields 4.44%. I can’t see how the Flux’s USDC market will feed the demand for borrowing against OUSG. Earning 4.44% is now quite common in deFi, so there is a difficult-to-bridge gap between the incentive for both parties to use Flux. The utilization rate will likely be pushed to extreme levels. The underlying rate (supply apy) should therefore remain at least at this level or increase seriously.

Thank you for your time and sorry for the typos, redundancies and various heresies, they will be corrected if I find them (tell me).

Pendle is a titan. This is not financial advice.

References : Pendle whitepapers

- Pendle docs

- Pendle website

- Pendle audits

- Pendle medium